- Home

Edition

Africa Australia Brasil Canada Canada (français) España Europe France Global Indonesia New Zealand United Kingdom United States- Africa

- Australia

- Brasil

- Canada

- Canada (français)

- España

- Europe

- France

- Indonesia

- New Zealand

- United Kingdom

- United States

The AI sector is booming, but much of the investment is speculative.

(Saradasish Pradhan/Unsplash)

The AI bubble isn’t new — Karl Marx explained the mechanisms behind it nearly 150 years ago

Published: November 30, 2025 1.51pm GMT

Elliot Goodell Ugalde, Queen's University, Ontario

The AI sector is booming, but much of the investment is speculative.

(Saradasish Pradhan/Unsplash)

The AI bubble isn’t new — Karl Marx explained the mechanisms behind it nearly 150 years ago

Published: November 30, 2025 1.51pm GMT

Elliot Goodell Ugalde, Queen's University, Ontario

Author

-

Elliot Goodell Ugalde

Elliot Goodell Ugalde

PhD Candidate, Political Economy, Queen's University, Ontario

Disclosure statement

Elliot Goodell Ugalde does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

Partners

Queen's University, Ontario provides funding as a founding partner of The Conversation CA.

Queen's University, Ontario provides funding as a member of The Conversation CA-FR.

View all partners

DOI

https://doi.org/10.64628/AAM.xqmhy659t

https://theconversation.com/the-ai-bubble-isnt-new-karl-marx-explained-the-mechanisms-behind-it-nearly-150-years-ago-270663 https://theconversation.com/the-ai-bubble-isnt-new-karl-marx-explained-the-mechanisms-behind-it-nearly-150-years-ago-270663 Link copied Share articleShare article

Copy link Email Bluesky Facebook WhatsApp Messenger LinkedIn X (Twitter)Print article

When OpenAI’s Sam Altman told reporters in San Francisco earlier this year that the AI sector is in a bubble, the American tech market reacted almost instantly.

Combined with the fact that 95 per cent of AI pilot projects fail, traders treated his remark as a broader warning. Although Altman was referring specifically to private startups rather than publicly traded giants, some appear to have interpreted it as an industry-wide assessment.

Tech billionaire Peter Thiel sold his Nvidia holdings, for instance, while American investor Michael Burry (of The Big Short fame) has made million-dollar bets that companies like Palantir and Nvidia will drop in value.

What Altman’s comment really exposes is not only the fragility of specific firms but the deeper tendency Prussian philosopher Karl Marx predicted: the problem of surplus capital that can no longer find profitable outlets in production.

OpenAI CEO Sam Altman recently told reporters he believes the AI sector is in a bubble. Altman speaks at the Federal Reserve in Washington, D.C., in July 2025.

(AP Photo/Mark Schiefelbein)

OpenAI CEO Sam Altman recently told reporters he believes the AI sector is in a bubble. Altman speaks at the Federal Reserve in Washington, D.C., in July 2025.

(AP Photo/Mark Schiefelbein)

Marx’s theory of crisis

The future of AI is not in question. Like the internet after the dot-com crash, the technology will endure. What is in question is where capital will flow once AI equities stop delivering the speculative returns they have promised over the past few years.

That question takes us directly back to Marx’s analysis of crises driven by over-accumulation. Marx argued that an economy becomes unstable when the mass of accumulated capital can no longer be profitably reinvested.

An overproduction of capital, he explained, occurs whenever additional investment fails to generate new surplus value. When surplus capital cannot profitably be absorbed through the production of goods, it is displaced into speculative outlets.

Tech investments mask economic weakness

Years of low interest rates and pandemic-era liquidity have swollen corporate balance sheets. Much of that liquidity has entered the technology sector, concentrating in the so-called “Magnificent Seven” — Amazon, Alphabet, Meta, Apple, Microsoft, Nvidia and Tesla. Without these firms, market performance would be negative.

Nvidia CEO Jensen Huang speaks about how AI infrastructure and AI factories are powering a new industrial revolution, at Washington Convention Center in October 2025 in Washington, D.c.

(AP Photo/Manuel Balce Ceneta)

Nvidia CEO Jensen Huang speaks about how AI infrastructure and AI factories are powering a new industrial revolution, at Washington Convention Center in October 2025 in Washington, D.c.

(AP Photo/Manuel Balce Ceneta)

This does not signal technological dynamism; it reflects capital concentrated in a narrow cluster of overvalued assets, functioning as “money thrown into circulation without a material basis in production” that circulates without any grounding in real economic activity.

The consequence of this is that less investment reaches the “real economy”, which fuels economic stagnation and the cost-of-living crisis, both of which remain obscured by the formal metric of GDP.

How AI became the latest fix

Economic geographer David Harvey extends Marx’s insight through the idea of the “spatio-temporal fix,” which refers to the way capital temporarily resolves stagnation by either pushing investment into the future or expanding into new territories.

Over-accumulation generates surpluses of labour, productive capacity and money capital, which cannot be absorbed without loss. These surpluses are then redirected into long-term projects that defer crises into new spaces that open fresh possibilities for extraction.

The AI boom functions as both a temporal and a spatial fix. As a temporal fix, it offers investors claims on future profitability that may never arrive — what Marx called “fictitious capital.” This is wealth that shows up on balance sheets despite having little basis in the real economy rooted in the production of goods.

Read more: Yes, there is an AI investment bubble – here are three scenarios for how it could end

Spatially, the expansion of data centres, chip manufacturing sites and mineral extraction zones requires enormous physical investment. These projects absorb capital while depending on new territories, new labour markets and new resource frontiers.

Yet as Altman’s admission suggests, and as U.S. President Donald Trump’s protectionist measures complicate global trade, these outlets are reaching their limits.

The costs of speculative capital

The consequences of over-accumulation extend far beyond firms and investors. They are experienced socially, not abstractly. Marx explained that an overproduction of capital corresponds to an overproduction of the means of production and necessities of life that cannot be used at existing rates of exploitation.

In other words, stagnant purchasing power prevents capital from being valorized at the pace it is being produced. As profitability declines, the economy resolves the imbalance by destroying the livelihoods of workers and households whose pensions are tied to equities.

History offers stark examples. The dot-com crash wiped out small investors and concentrated power in surviving firms. The 2008 financial crisis displaced millions from their homes while financial institutions were rescued.

Today, large asset managers are already hedging against potential turbulence. Vanguard, for instance, has shifted significantly toward fixed income.

Speculation drives growth

The AI bubble is primarily a symptom of structural pressures rather than purely a technological event. In the early 20th century, Marxist economist Rosa Luxemburg questioned where the continually increasing demand required for expanded reproduction would come from.

Her answer echoes Marx and Harvey: when productive outlets shrink, capital moves either outward or into speculation. The U.S. increasingly chooses the latter.

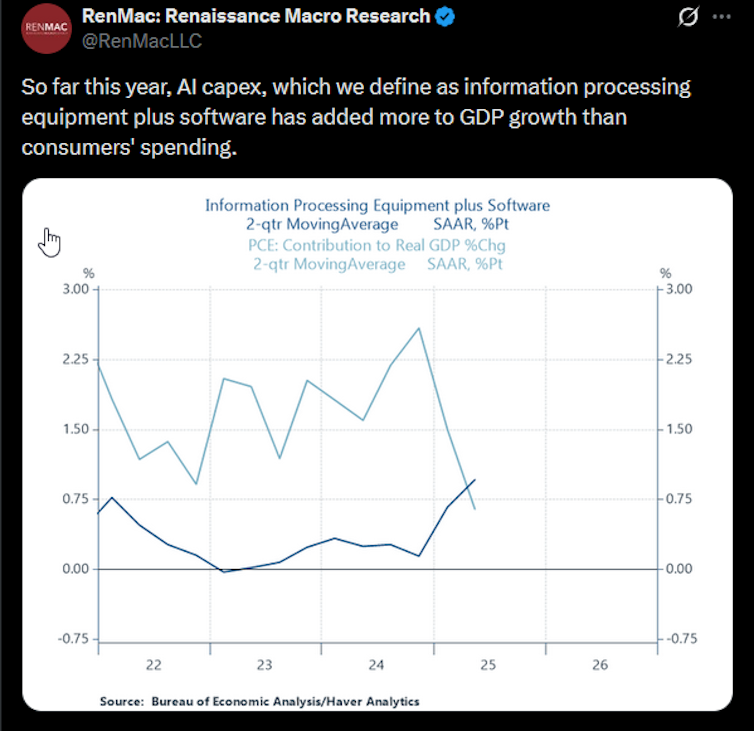

Corporate spending on AI infrastructure now contributes more to GDP growth than household consumption, an unprecedented inversion that shows how much growth is being driven by speculative investment rather than productive expansion.

This dynamic pulls down the rate of profit, and when the speculative flow reverses, contraction will follow.

(X/Twitter)

(X/Twitter)

Tariffs tighten the squeeze on capital

Financial inflation has intensified as the traditional pressure valves that once allowed capital to move into new physical or geographic markets have narrowed.

Tariffs, export controls on semiconductors and retaliatory trade measures have narrowed the global space available for relocation. Since capital cannot readily escape the structural pressures of the domestic economy, it increasingly turns to financial tools that postpone losses by rolling debt forward or inflating asset prices; mechanisms that ultimately heighten fragility when the reckoning comes.

U.S. Federal Reserve Chair Jerome Powell’s openness to interest rate cuts signals a renewed turn toward cheap credit. Lower borrowing costs let capital paper over losses and pump up fresh speculative cycles.

Federal Reserve Chairman Jerome Powell speaks at a news conference after the Federal Open Market Committee meeting in October 2025 at the Federal Reserve Board Building in Washington, D.C.

(AP Photo/Manuel Balce Ceneta)

Federal Reserve Chairman Jerome Powell speaks at a news conference after the Federal Open Market Committee meeting in October 2025 at the Federal Reserve Board Building in Washington, D.C.

(AP Photo/Manuel Balce Ceneta)

Marx captured this logic in his analysis of interest-bearing capital, where finance generates claims on future production “above and beyond what can be realized in the form of commodities.”

The result is that households are pushed to take on more debt than they can manage, effectively swapping a crisis of stagnation for a crisis of consumer credit.

Bubbles and social risk

If the AI bubble bursts when governments have limited room to shift investment internationally and the economy is propped up by increasingly fragile credit, the consequences could be serious.

Capital will not disappear, but will instead concentrate in bond markets and credit instruments inflated by a U.S. central bank eager to cut interest rates. This does not avert crisis; it merely transfers the costs downward.

Bubbles are not accidents, but recurring mechanisms for absorbing surplus capital. If Trump’s protectionism ensures that spatial outlets continue to close and temporal fixes rely on ever riskier leverage, the system moves toward a cycle of asset inflation, collapse and renewed state intervention.

AI will survive, but the speculative bubble surrounding it is a sign of a deeper structural problem — the cost of which, when finally realized, will fall most heavily on the working class.

- Artificial intelligence (AI)

- Investing

- Karl Marx

- Dot-com bust

- AI bubble

Events

Jobs

-

Lecturer/Senior Lecturer - Electrical Engineering

Lecturer/Senior Lecturer - Electrical Engineering

-

University Lecturer in Early Childhood Education

-

Case Specialist, Student Information and Regulatory Reporting

-

Lecturer in Paramedicine

-

Associate Lecturer, Social Work

- Editorial Policies

- Community standards

- Republishing guidelines

- Analytics

- Our feeds

- Get newsletter

- Who we are

- Our charter

- Our team

- Partners and funders

- Resource for media

- Contact us

-

-

-

-

Copyright © 2010–2025, The Conversation